H'lala

A case study about the design of Shariah compliant Fintech bank platform

Background information

WHAT IS H'LALA?

In a wave of Fintech startups such as Monzo & Starling, one customer is still underserved. None of the Fintech ventures are Shariah compliant, so would be unsuitable for members of the Mulsim faith. H'lala is on a mission to create the first compliant bank aiming to serve this beachhead.

Islamic banks in the UK offer Islamic current accounts, as do a small number of mainstream banks. These accounts are similar to traditional current accounts but there's no credit or debit interest, no planned overdraft, no minimum balance requirement and no charges for transactions. However, this means that if you try to make a transaction that would send your account overdrawn, the transaction might be rejected and you might be charged an unpaid item fee. The money kept in Islamic bank accounts with UK banks has to be ring-fenced and not used for any interest-based or non-Sharia approved activities.

Islamic banks in the UK offer Islamic current accounts, as do a small number of mainstream banks. These accounts are similar to traditional current accounts but there's no credit or debit interest, no planned overdraft, no minimum balance requirement and no charges for transactions. However, this means that if you try to make a transaction that would send your account overdrawn, the transaction might be rejected and you might be charged an unpaid item fee. The money kept in Islamic bank accounts with UK banks has to be ring-fenced and not used for any interest-based or non-Sharia approved activities.

THE PROBLEM

H'lala do not have the advantage of being first to the Fintech market, however they do have the bonus of being only one of two companies looking to offer products for Muslims. Islamic banking refers to banking which is in accordance with Sharia law and its application in Islamic economics. However, although Islamic banks and current accounts follow Sharia financial rules, they're open to everybody, regardless of religious belief.

Current banking providers such as Natwest, Lloyds, Barclays are not Shariah compliant as they make interest on their products.

Instead of charging interest, Islamic banks make money by using contracts that are allowed under Sharia law, including leasing contracts, sale contracts and partnership contracts. So instead of lending you the money to buy a car or house, an Islamic bank might buy the product and allow a customer to buy it from them - for an increased price - by paying instalments over time.

In April 2014 Lloyds Bank stopped charging interest on overdrafts for customers with Islamic bank accounts. Lloyds Bank wrote to all its customers to inform them that it was removing a fee of £6 a month for people who went into an unplanned overdraft, but only for its Islamic accounts.

Some non-Muslim customers claimed they were being discriminated against by being forced to pay fees which Muslim customers didn't have to pay, but Islamic bank accounts aren't available to just Muslim customers - anyone can open an Islamic account.

Current banking providers such as Natwest, Lloyds, Barclays are not Shariah compliant as they make interest on their products.

Instead of charging interest, Islamic banks make money by using contracts that are allowed under Sharia law, including leasing contracts, sale contracts and partnership contracts. So instead of lending you the money to buy a car or house, an Islamic bank might buy the product and allow a customer to buy it from them - for an increased price - by paying instalments over time.

In April 2014 Lloyds Bank stopped charging interest on overdrafts for customers with Islamic bank accounts. Lloyds Bank wrote to all its customers to inform them that it was removing a fee of £6 a month for people who went into an unplanned overdraft, but only for its Islamic accounts.

Some non-Muslim customers claimed they were being discriminated against by being forced to pay fees which Muslim customers didn't have to pay, but Islamic bank accounts aren't available to just Muslim customers - anyone can open an Islamic account.

MY ROLE

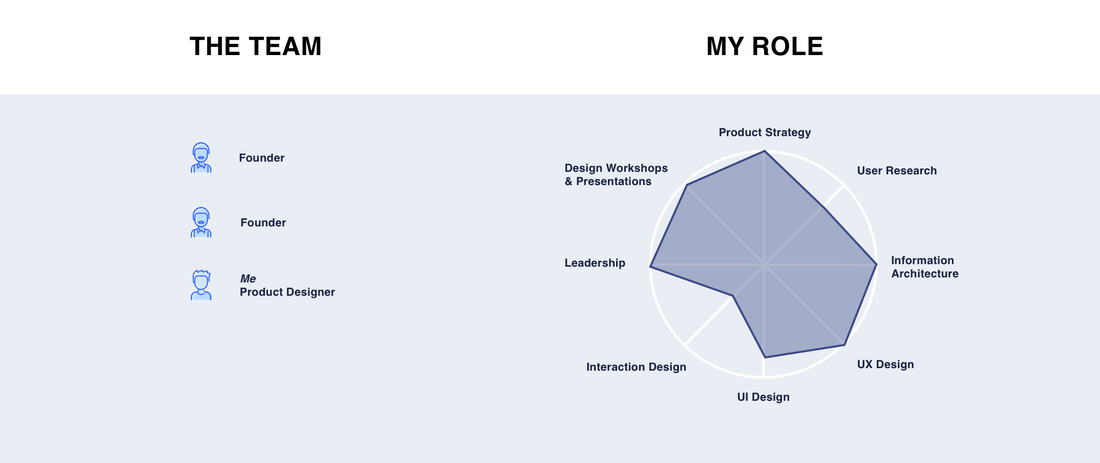

I was approached in 2019 by the two founders of H'lala to take their product idea and turn it into something tangible. They had completed their market research, to a high level and were ready to take the next leap, to commission the full design of their brand and app design, which they could then put infront of investors to showcase their proposal and raise some capital to grow their business.

I would help the H'lala team of two develop their branding, and completely design their app architecture, ending in providing a fully tested clickable prototype.

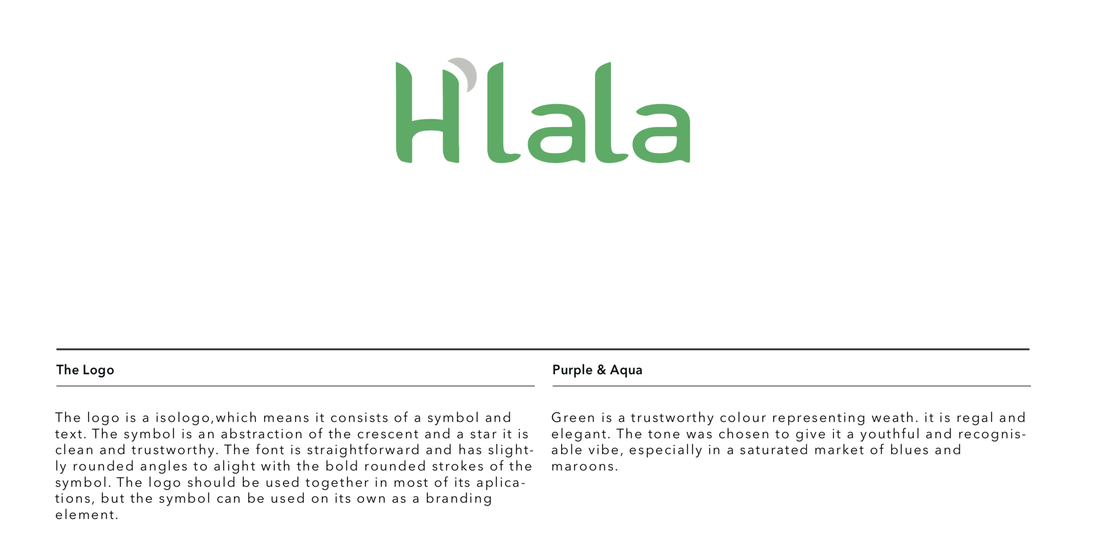

Alongside the logo, the colour palette went through various different iterations shifting the colour focus from a deep green and gold, to a softer subtler WhatsApp blended colour.

I would help the H'lala team of two develop their branding, and completely design their app architecture, ending in providing a fully tested clickable prototype.

Alongside the logo, the colour palette went through various different iterations shifting the colour focus from a deep green and gold, to a softer subtler WhatsApp blended colour.

Over the course of a few weeks the brand was defined and the logo mark was agreed by myself and the stakeholders.

CARD DESIGN

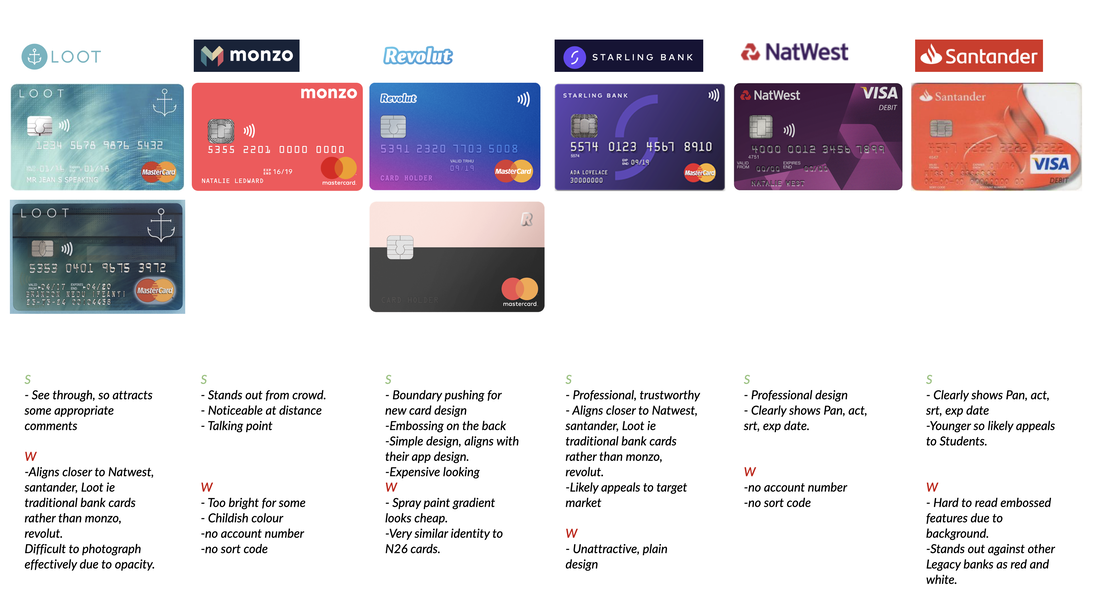

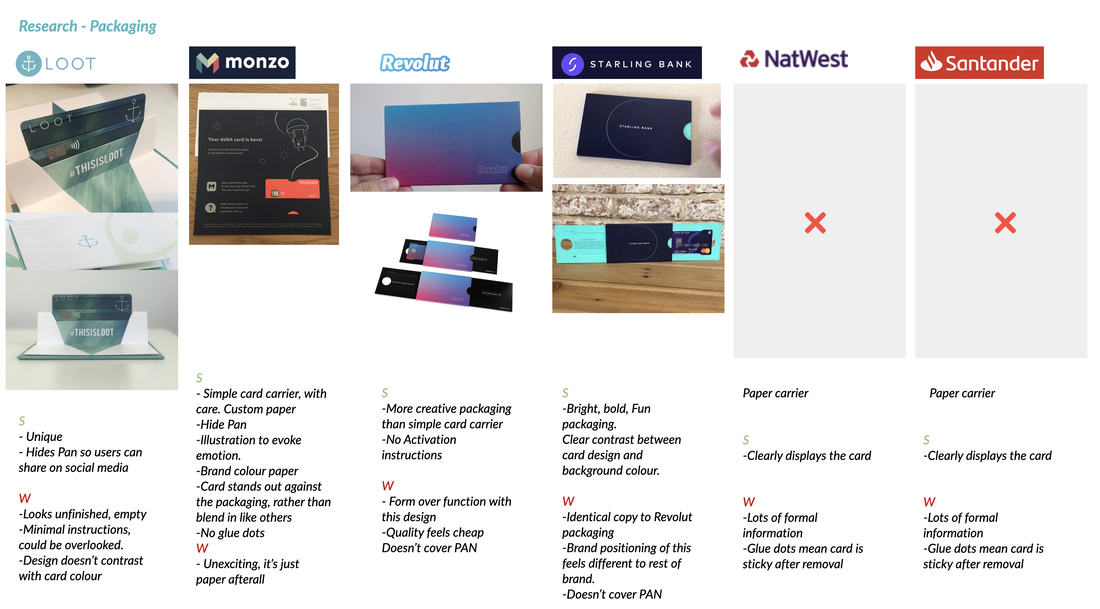

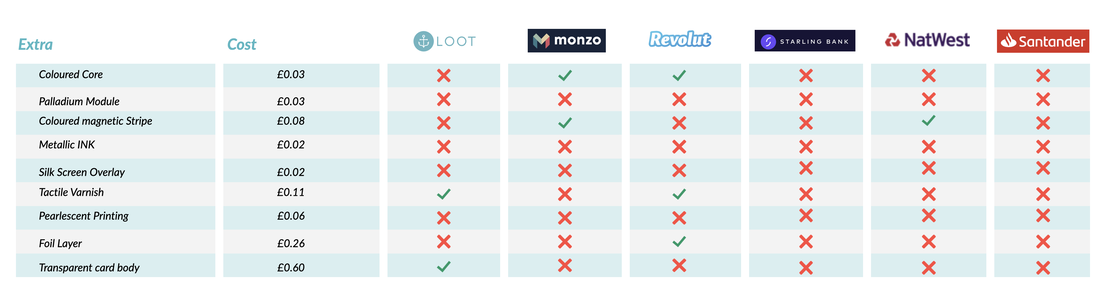

After we had secured the logo design and colour palette, we started working on the visual design for the bank card. The bank card for a bank can be the only tangible element the customer has the opportunity to interact with. I started doing a UX teardown/competitor analysis of all the competitor card makeups highlighting pro's and con's.

Not only did I look at how the card was presented, but also how it was delivered. Many new digital banks have attempted to create delightful moments when a users card arrives, aiding to create an emotional connection between the user and the brand. While these creative packaging examples can add to total CPA cost, by prompting them to be sharable content, these quick packaging methods could ultimately decrease your acquisition cost by creating a viral sensation.

Cost can also be a huge focus when designing a new debit card, and for H'lala should be integral to any design decisions made. This is important because, let's say one card costs £2.00 including printing, PERSO, shipping and packaging, if you issue 250,000 cards, that's a total cost of £500k, just to get the cards into the hands of the onboard customers.

After numerous meetings with the co-founders we filtered through a variety of different card design iterations before landing on the initial designs. One concept the founders wanted to move through was to have a number of subscription tiers for different banking products. This meant a family of card designs would need tone created, each made of slightly different materials.

The H'lala card design is about more than just making the card stand out; it’s about finding a better way of doing things, being responsive to cultural and technological shifts and adapting to them. Our lives are largely lived in portrait now, think about how you hold your phone or tap your current bank card.

H'lala is focussed on disrupting the norm, and by implementing a portrait card, they are beginning todo that!

H'lala is focussed on disrupting the norm, and by implementing a portrait card, they are beginning todo that!

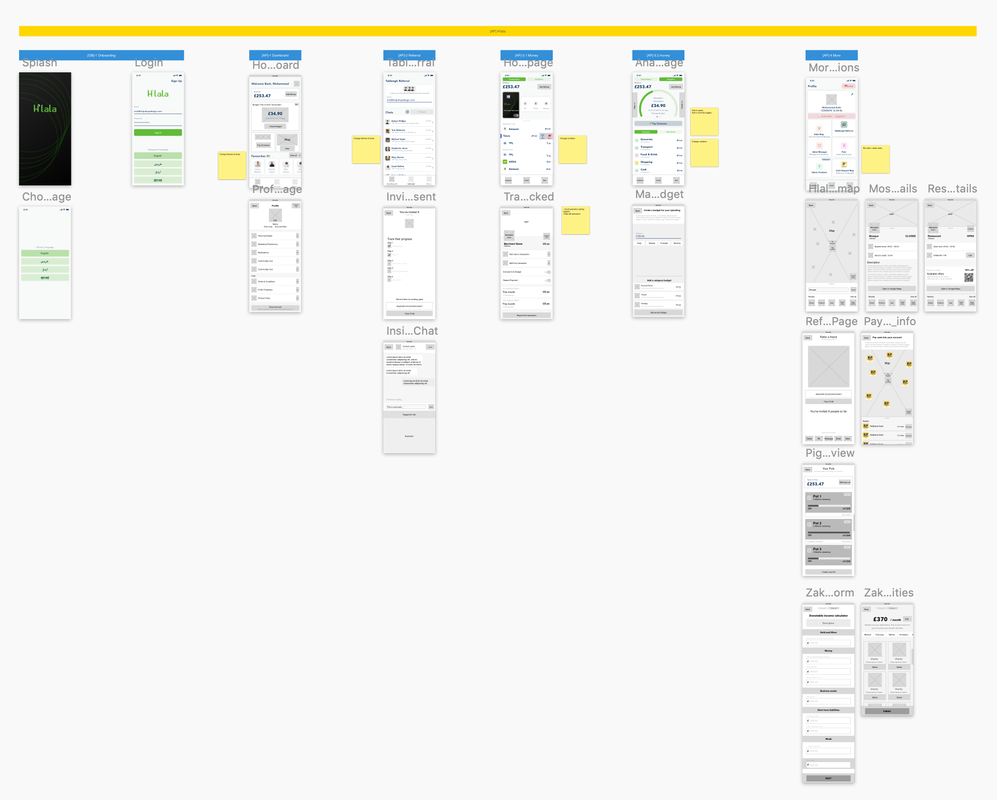

WIREFRAMING THE SOLUTION

Once the card design was finalised, I started taking the ideas the founders had detailed and started turning them into wireframes, using UX principles to influence my content decision making. The key areas the team wanted to focus on were:

-Key banking features for competitor parity (direct debits, digital KYC)

-Shariah product offering

-Key banking features for competitor parity (direct debits, digital KYC)

-Shariah product offering

Once we had solidified the wireframes and the user journeys it was time to get some early feedback through some user testing. For this we decided to test with people who follow the teachings of Islam, and those that didn't. This would help us better understand how the products we listed were percieved and explained to an adequate level for everyone using the product.

From out user interviews we had a couple of iterations needed to quite a few steps in the journey. This included smaller things like additional descriptions or button prompts, through to larger architecture movements such as adding an additional feature to the tab bar navigation.

After the second wave of iterations were executed we locked in the wireframes and pushed forward to the UI design phase.

Features included:

-Chat function for 24/7 support

-Halal restaurant locator

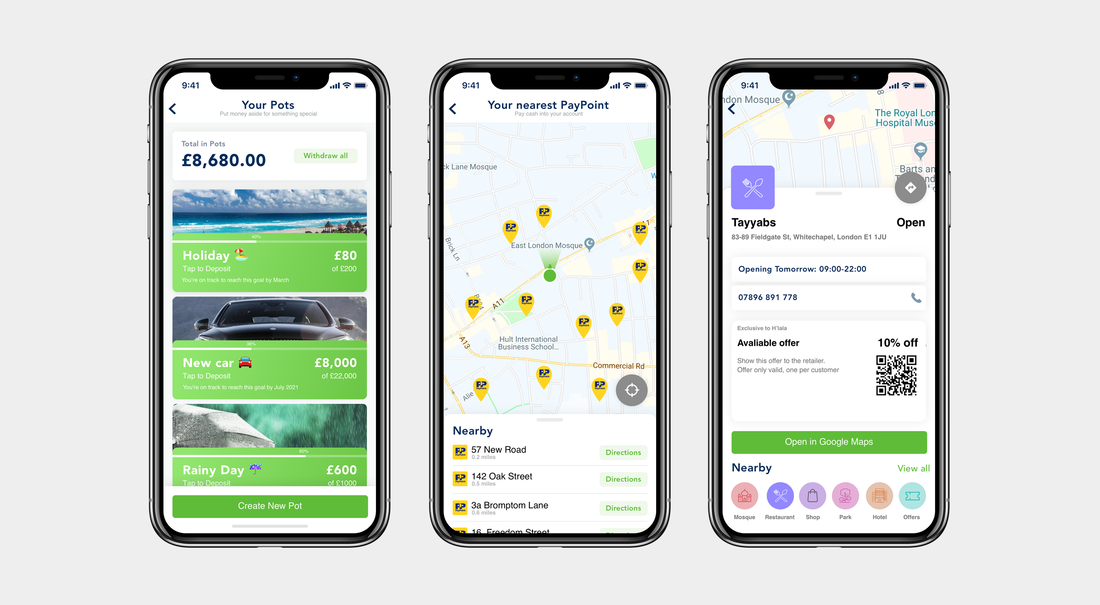

-Money management features

-Shariah savings goals, to be placed in investments.

-Transaction details for merchants

Features included:

-Chat function for 24/7 support

-Halal restaurant locator

-Money management features

-Shariah savings goals, to be placed in investments.

-Transaction details for merchants

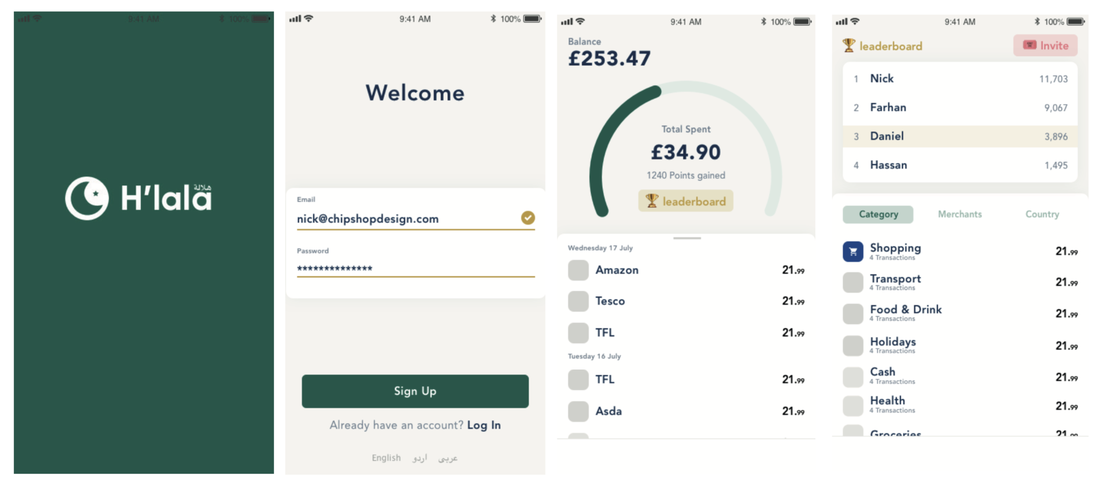

HI-FI DESIGN

The wireframes were progressing alongside the branding elements so for the initial Hi-Fi designs I produced these in the current branding direction, which would later change.

The Hi-Fi designs developed much more once the branding was confirmed, and really began to form it's own individual identity unique to H'lala. The visual style is similar to that of Revolut in terms of Dieter Rams' less is more inspired interface. The strong brand colour, and WCAG approved green ensures all icons and elements are usable.

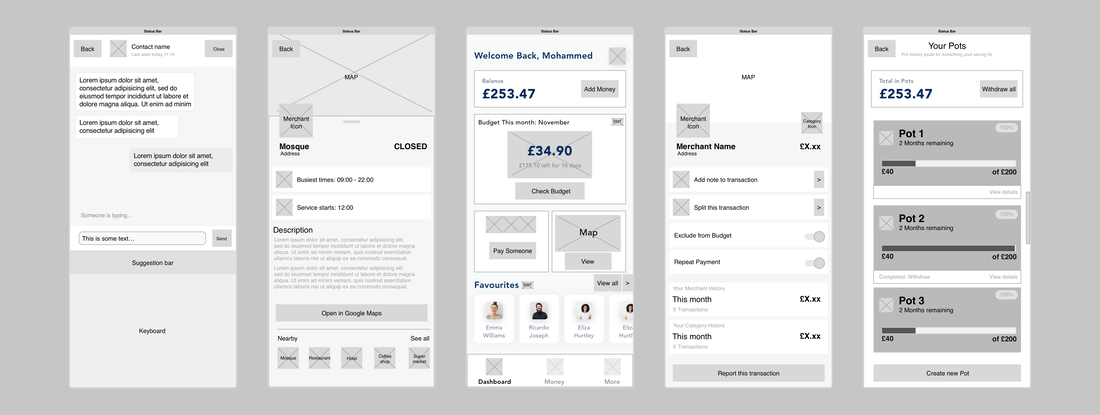

FEATURES

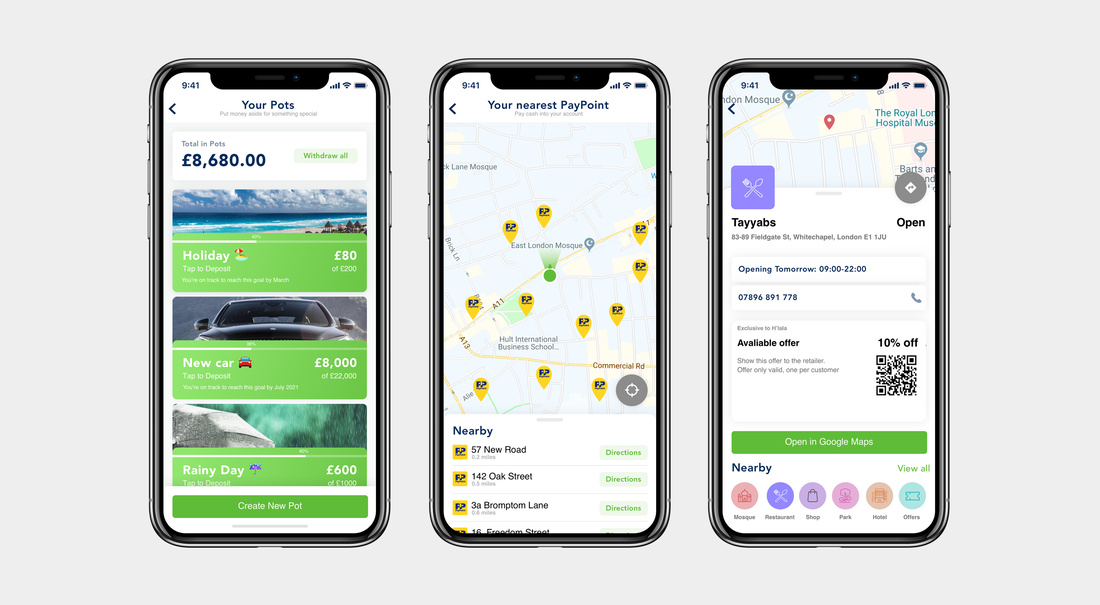

Three features that on the surface felt similar to those of Monzo, Pockit, and Revolut were a PayPal location map, a transaction details view, and a savings goal.

Despite feeling like competitor products, behind the scenes these features are required to act differently.

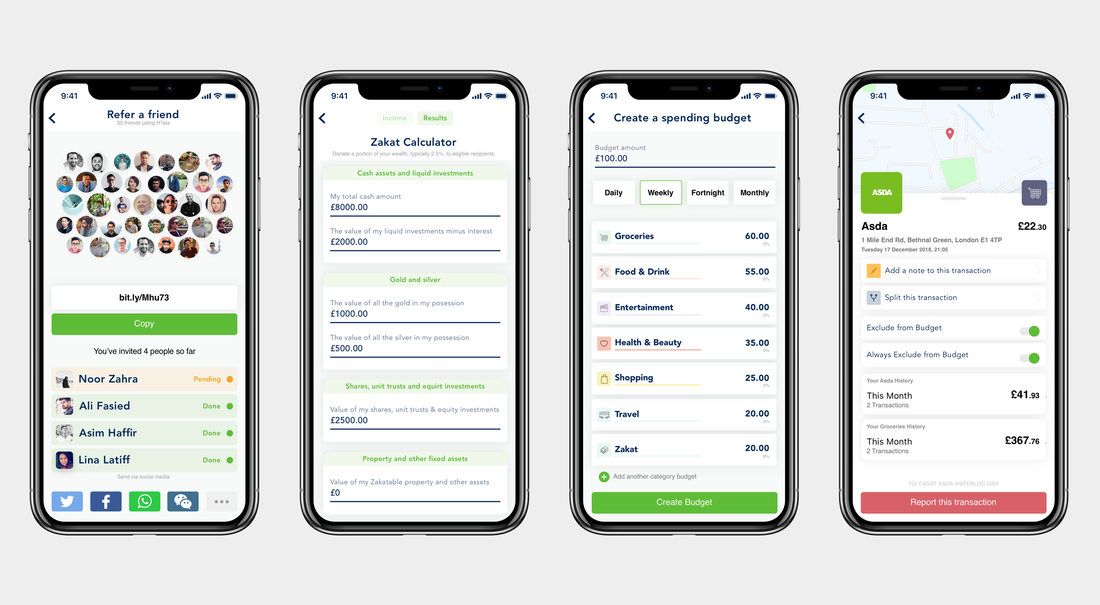

Let's take the savings goal feature which need to comply with Sharia law, this means any money from Islamic savings must be invested instead of lent out and isn't used for any investment which isn't in accordance with Sharia law, ruling out things like tobacco, alcohol and gambling.

Ijara is a leasing arrangement, sometimes called a house purchase plan (HPP) in the case of mortgages. It involves the bank buying a house, car or other goods for a customer, then leasing it back to them. Each lease payment contains an instalment towards the purchase price of the commodity, so eventually the customer will own the property outright. Until that point, the bank remains the legal owner.

Another feature which differs slightly is the transaction details view, which looks to merge the gap between Google maps, and your bank account. The H'lala account would indicate to the user any discount offers or if the restaurant is Halal.

Despite feeling like competitor products, behind the scenes these features are required to act differently.

Let's take the savings goal feature which need to comply with Sharia law, this means any money from Islamic savings must be invested instead of lent out and isn't used for any investment which isn't in accordance with Sharia law, ruling out things like tobacco, alcohol and gambling.

Ijara is a leasing arrangement, sometimes called a house purchase plan (HPP) in the case of mortgages. It involves the bank buying a house, car or other goods for a customer, then leasing it back to them. Each lease payment contains an instalment towards the purchase price of the commodity, so eventually the customer will own the property outright. Until that point, the bank remains the legal owner.

Another feature which differs slightly is the transaction details view, which looks to merge the gap between Google maps, and your bank account. The H'lala account would indicate to the user any discount offers or if the restaurant is Halal.

Zakat is one of the five pillars of Islam. It is a compulsory donation to charity by all Muslims who reach the minimum threshold for payment. There are many calculators online, but no islamic banks provide one in their applications. H'lala would integrate a thorough Zakat calculator and inform the user how much they are eligible to contribute.

PROTOTYPE

The final output for this project was to provide the founders with a set of designs which could then be handed to a developer. The secondary action for the project is to help the founders raise investment for the business.

TL;DR

I followed the double diamond UX approach to validate and design a brand and full banking app for a Fintech startup targeting the islamic banking market.